Vidhi Lalchand

Postdoctoral Fellow, Broad and MIT

Jan-Feb 2021

Fergus Simpson, Vidhi Lalchand, Carl E. Rasmussen

Background: Gaussian Processes

Gaussian Processes offer a powerful, Bayesian, non-parametric paradigm for learning functions.

Background: Gaussian Processes

Gaussian Processes offer a powerful, Bayesian, non-parametric paradigm for learning functions.

Conventionally, learning occurs via maximisation of the marginal likelihood

Objectives

Objectives

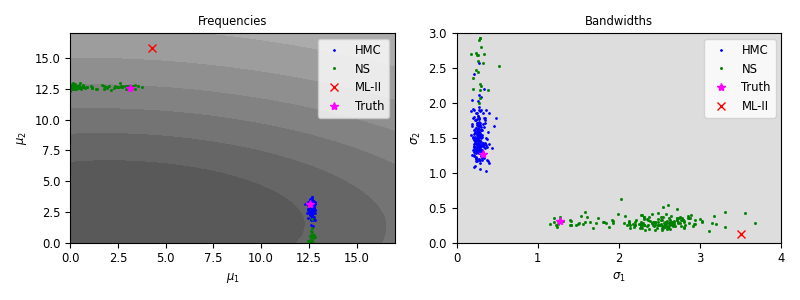

Learning with Spectral Mixture Kernels

Learning with Spectral Mixture Kernels

Marginalised Gaussian Processes

Generative Model

Marginalised Gaussian Processes

Generative Model

Predictions

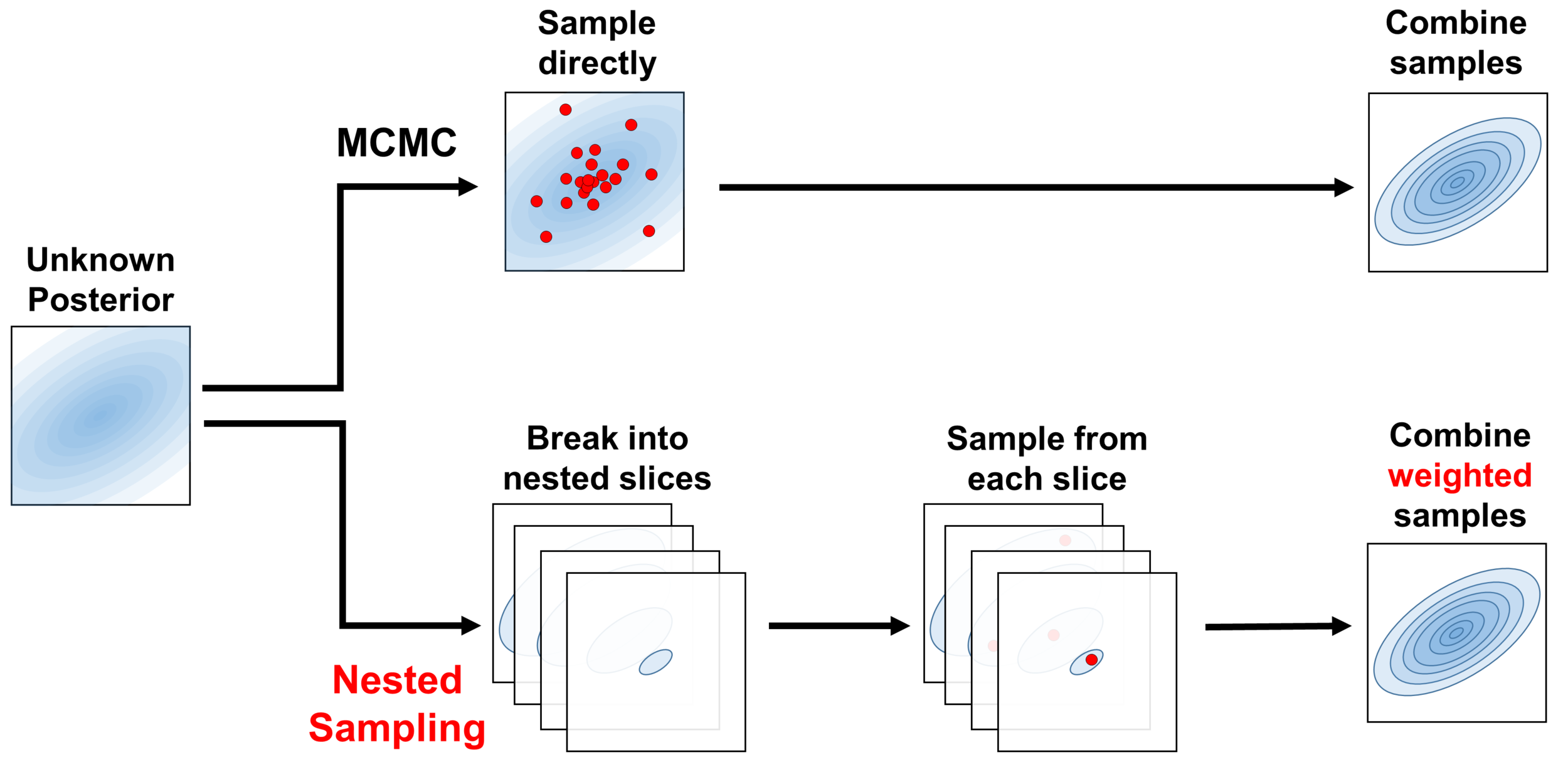

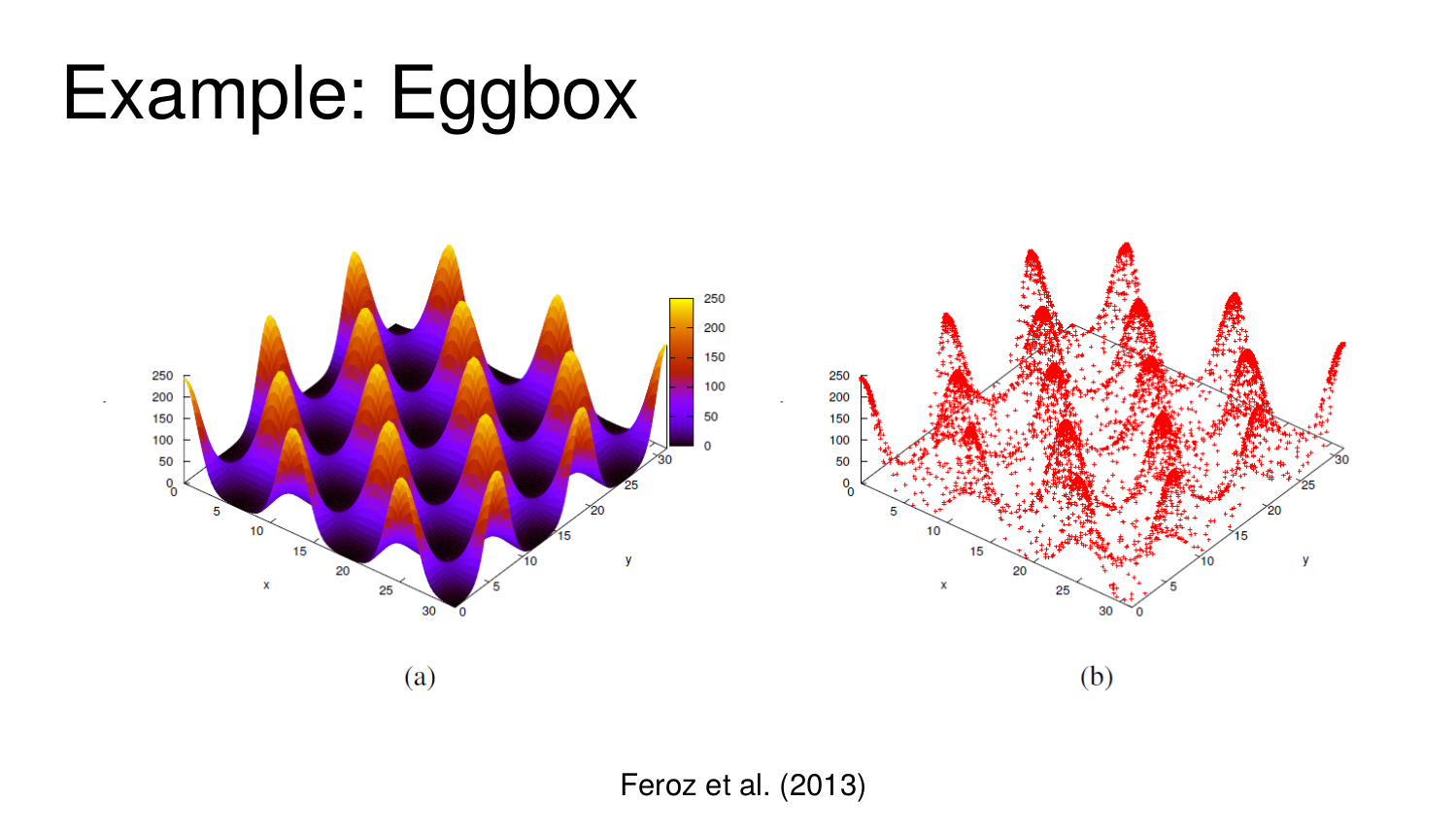

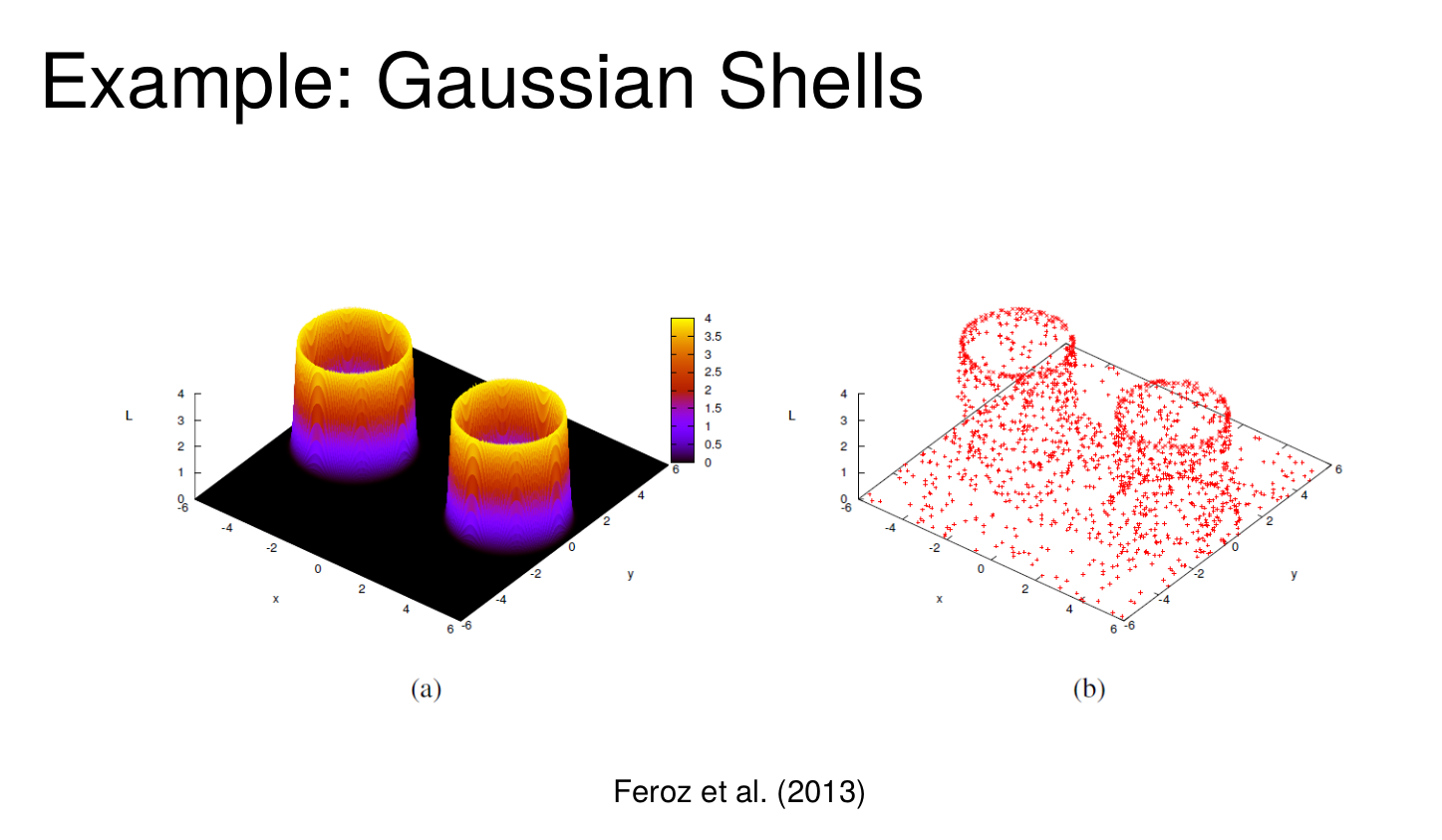

Overview: Nested Sampling

Speagle JS. dynesty: a dynamic nested sampling package for estimating Bayesian posteriors and evidences. Monthly Notices of the Royal Astronomical Society. 2020 Apr;493(3):3132-58.

Overview: Nested Sampling

Speagle JS. dynesty: a dynamic nested sampling package for estimating Bayesian posteriors and evidences. Monthly Notices of the Royal Astronomical Society. 2020 Apr;493(3):3132-58.

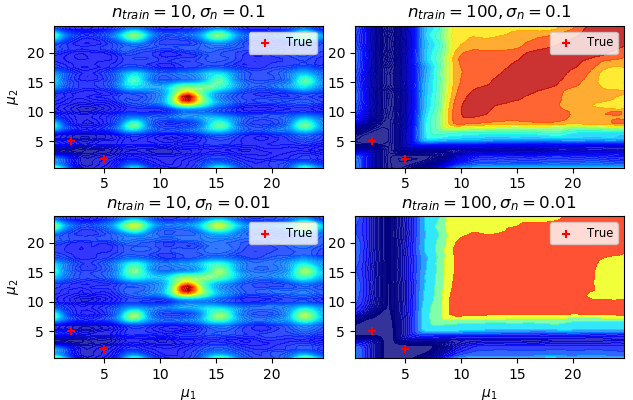

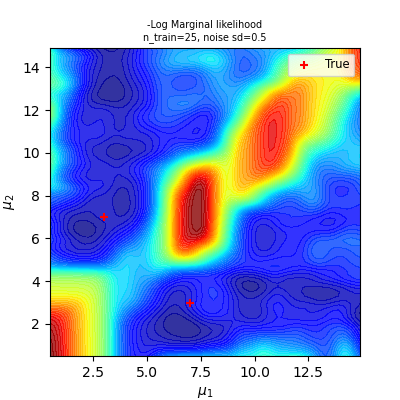

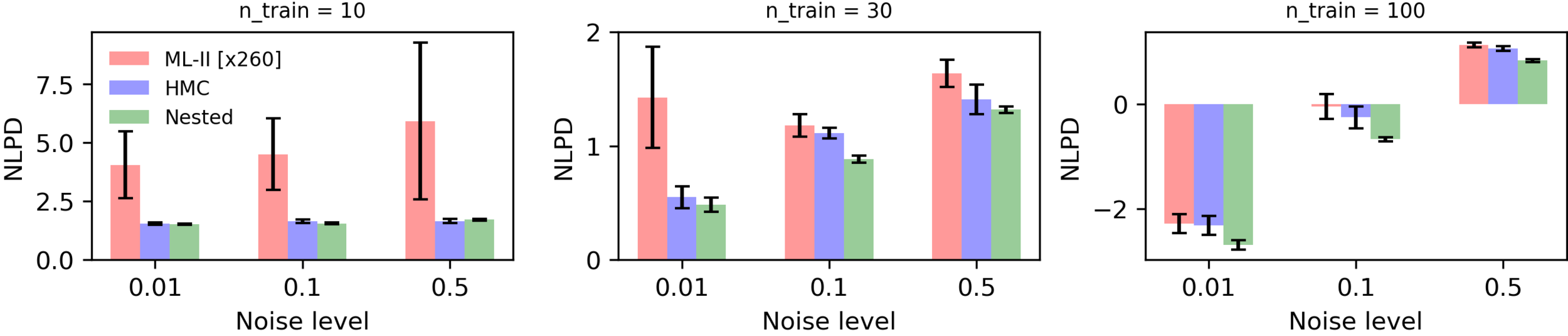

Synthetic Experiments

Synthetic Experiments

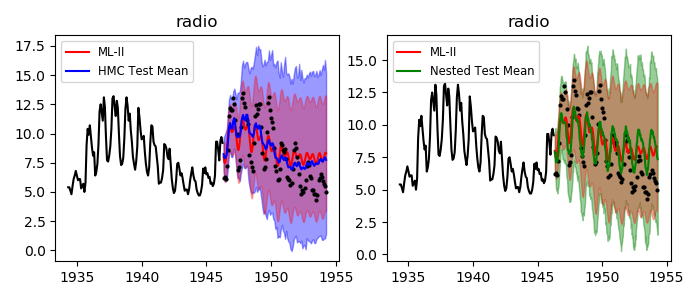

Time-series prediction (1d)

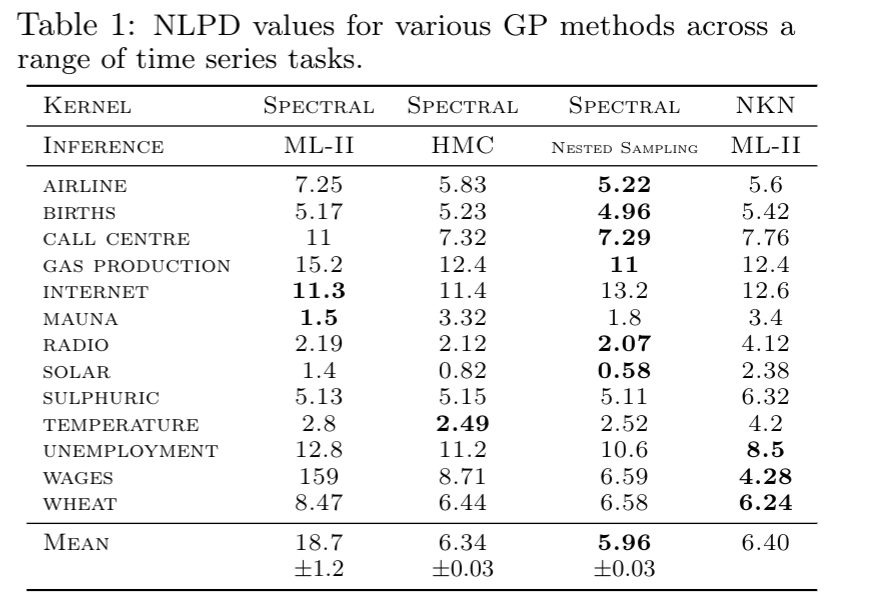

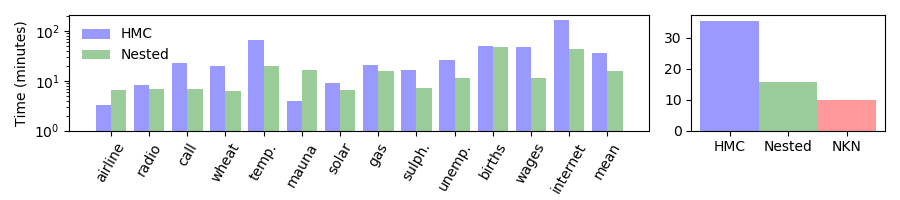

Time series benchmarks

Time series benchmarks

Time-series prediction (1d)

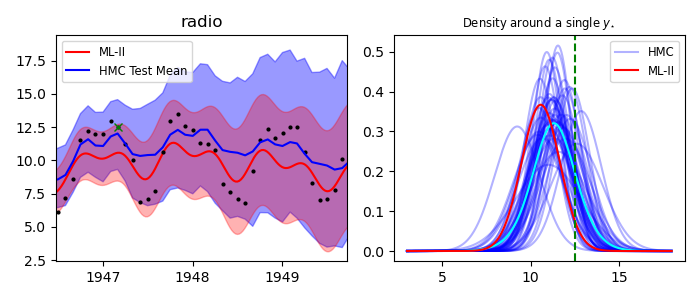

Why is it better?

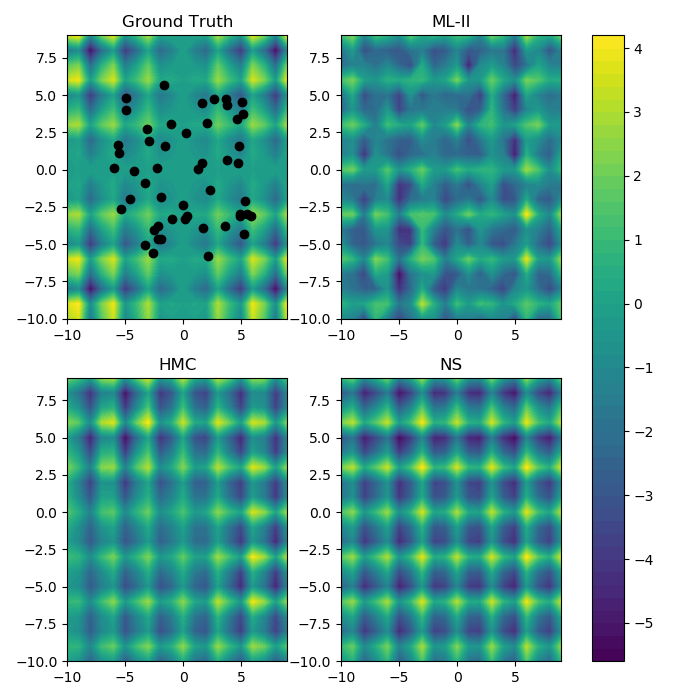

Pattern Prediction (2d)

Train: 50 points chosen randomly and uniformly between [-6 x 6] grid.

Test: [-10 x 10] grid of 400 points.

NLPD

ML-II: 216

Hamiltonian Monte Carlo: 2.56

Nested Sampling : 2.62

Summary

Summary

Marginalised GPs give robust prediction intervals by accounting for hyperparameter uncertainty. Their advantage over ML-II become particularly pronounced when expressive kernels with several hyperparameters are used or where the training data is either sparse or noisy.

Thank you!

By Vidhi Lalchand