Book 4. Liquidity and Treasury Risk

FRM Part 2

LTR 14. Liquidity Transfer Pricing

Presented by: Sudhanshu

Module 1. Best Practices and Challenges for Liquidity Transfer Pricing

Module 2. Approaches for Liquidity Transfer Pricing and Contingent Liquidity Liquidity Risk Pricing

Module 1. Best Practices and Challenges for Liquidity Transfer Pricing

Topic 1. LTP Process

Topic 2. Major Shortcomings Prior to the GFC

Topic 3. Centralized Management of LTP Process

Topic 4. Need for Strong Governance in LTP Process

Topic 5. Best Practices for Governing the LTP Process

Topic 6. Lessons from Governance Failures in GFC

Topic 7. Challenges of Implementing the LTP Process

Topic 1. LTP Process

-

Definition of LTP: Liquidity Transfer Pricing (LTP) allocates the costs, benefits, and risks of liquidity to the appropriate business units within a bank.

-

Centralized governance: LTP should be centrally managed by the group treasury to ensure consistency and control across the bank.

-

Pricing basis: Liquidity funding rates should be attributed using the bank’s marginal cost of funds, matched to the maturity of the underlying product.

-

Reference curves:

-

Historically based on the LIBOR/swap curve

-

Transitioning to alternative reference rates such as SOFR

-

-

Treatment of loans (assets):

-

Business units are charged a liquidity premium reflecting the cost of funding

-

Includes charging credit lines based on expected liquidity usage when fully drawn

-

-

Treatment of deposits (liabilities):

-

Business units are credited for providing liquidity

-

Credits depend on the maturity profile of deposits

-

-

Weak governance and controls: Decentralized funding structures and weak internal risk controls required manual LTP adjustments, leading to poor management and risk oversight.

-

Inadequate LMIS granularity: Liquidity management information systems failed to measure liquidity costs, benefits, and risks at a detailed business-unit level.

-

Misaligned incentives: Employees and managers were rewarded on overstated profits that ignored true liquidity funding costs and risks.

-

Flawed LTP methodologies: Zero-cost and average-cost funding approaches underpriced liquidity for illiquid long-term assets and failed to reward liquidity providers.

-

Insufficient stress testing: Stress tests were not used to size liquidity buffers for off-balance-sheet contingencies or prolonged idiosyncratic and market stress.

-

Maturity mismatch in funding: Illiquid long-term assets were funded with overnight sources that proved unavailable in systemic crises, leading to underestimated liquidity costs.

-

Blunt liquidity charges: Uniform average charges and small liquidity premiums ignored business-unit-specific contingent liquidity risks.

Topic 2. Major Shortcomings Prior to the GFC

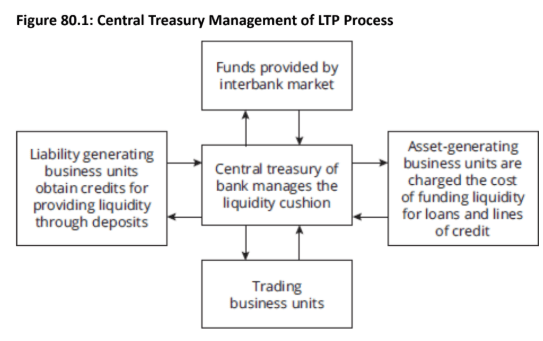

- Fig 80.1 shows a centralized approach for managing the LTP process.

-

The entire wholesale funding is transferred through the central treasury.

-

Loan and deposit liquidity pricing: The central treasury charges loan-originating business units for funding liquidity costs and credits business units that provide liquidity through deposits.

-

Trading usage charges: Trading desks are charged for using funds related to contingent commitments such as derivatives exposures and collateral calls.

-

Trading funding credits: Trading business units receive credits when they provide liquidity by selling marketable securities.

Topic 3. Centralized Management of LTP Process

Topic 4. Need for Strong Governance in LTP Process

-

Prevents balance-sheet illiquidity: Effective LTP discourages banks from overweighting their balance sheets with illiquid assets.

- Supports maturity matching: LTP should align asset maturities with liability maturities, ensuring an adequate liquidity cushion

- Correct liquidity pricing: Weak LTP frameworks underprice or fail to price the true cost or benefit of liquidity.

-

Behavioral incentives: Poor LTP creates incentives for business units to accumulate illiquid assets by mispricing liquidity.

-

External vs internal controls in LTP

-

LTP processes are influenced by external factors such as regulation and competition, which affect all banks similarly.

-

As a result, banks must place greater emphasis on internal controls, including board oversight and effective risk management.

-

-

Impact of weak internal controls

-

Institutions with weak internal controls tend to have poor LTP processes where liquidity is either not priced or significantly underpriced.

-

This mispricing leads to adverse selection in loan and deposit maturities and creates moral hazard in trading units that ignore liquidity costs and risks, including those from derivatives and contingent collateral calls.

-

Topic 5. Best Practices for Governing the LTP Process

-

Best Practices for Governing the LTP Process

-

Defined LTP framework: Banks should maintain a well-defined Liquidity Transfer Pricing (LTP) framework with clear principles and rules applicable across all business units that use or provide funding liquidity.

-

Centralized funding management: All wholesale funding should be centrally managed by the group treasury to ensure consistency and control.

-

Clear trading book policies: Funding policies and principles for the trading book must be clearly defined, understood, and monitored, with treasury having full visibility of funding liquidity risks.

-

Strong governance oversight: Senior management and independent risk and financial control functions should oversee the LTP process and meet monthly to review and monitor funding costs.

-

Granular cost attribution: The Liquidity Management Information System (LMIS) should allocate funding costs at a granular level, capturing all costs, benefits, and risks of funding liquidity for each business activity.

-

Incentive alignment: Employee compensation and bonus structures should incorporate liquidity costs to accurately reflect their impact on business unit profitability.

-

Practice Questions: Q1

Q1. Which of the following is considered a best practice of liquidity transfer pricing (LTP)?

A. A centralized treasury funding center should be implemented to manage the liquidity cushion across business units.

B. Banks should rely on external factors to improve LTP by meeting regulatory authority requirements.

C. Remuneration policies should not be linked to LTP to help incentivize business unit managers to produce longer-term assets.

D. Contingent collateral calls and derivatives should not be included in the LTP process but managed separately to properly account for risks.

Practice Questions: Q1 Answer

Explanation: A is correct.

A centralized funding center is necessary for proper internal governance of the LTP process. Wholesale funding should be restricted to a group or subsidiary treasury. Internal factors play an important role in effectively managing the LTP process. Proper LTP processes ensure remuneration policies are effective. LTP process must include contingent collateral calls and derivatives.

Topic 6. Lessons from Governance Failures in GFC

-

Centralized funding center is essential: Proper internal governance of the Liquidity Transfer Pricing (LTP) process requires a centralized funding center, typically within group or subsidiary treasury.

-

Risks of decentralized funding: Decentralized LTP structures often rely on manual, infrequently updated processes, leading to mispriced liquidity and internal arbitrage profits for business units.

-

-

Uncharged contingent liquidity risk: Banks with large trading operations frequently failed to charge business units for contingent liquidity exposures arising from derivatives and collateral calls.

-

Strong governance and oversight: Effective board oversight and risk controls are critical to prevent internal arbitrage and liquidity mispricing across business units.

-

Balance sheet maturity mismatches: Weak oversight allowed business units to accumulate long-term, illiquid assets funded by short-term liabilities, creating significant maturity mismatches.

-

Crisis-era funding failures: During the global financial crisis, short-term funding (overnight to 90-day) dried up, exposing banks holding illiquid assets such as highly rated CDOs to severe liquidity stress.

-

Unpriced margin call risk: The liquidity cost of potential margin calls was largely ignored prior to the crisis, and sharp market price declines triggered funding demands that many banks could not meet.

Topic 7. Challenges of Implementing the LTP Process

-

Oversight and governance: Implementing LTP requires strong oversight to monitor the process and prevent buildup of illiquid long-term assets caused by mispricing liquidity premiums, a key weakness exposed during the GFC.

-

Liquidity cost allocation: A major challenge is correctly charging business units for the cost of funding illiquid assets while crediting units that provide liquidity through deposits.

-

Centralized treasury model: A centralized treasury function is recommended over decentralized funding centers to reduce arbitrage opportunities and improve consistency in LTP outcomes.

-

Trading book liquidity risks: Effective LTP must incorporate policies and best practices to account for liquidity costs arising from derivatives, contingent funding needs, and margin or collateral calls.

-

Enterprise-wide involvement: Successful LTP implementation requires active participation from senior management, a central treasury function, and independent risk personnel, with more frequent (monthly) reviews of funding costs.

-

LMIS infrastructure: Robust LMIS capabilities are needed to deliver timely, high-quality liquidity reports and to track, price, and allocate liquidity costs, benefits, and risks to business units.

-

Performance and incentives alignment: Business unit performance measurement and executive remuneration must reflect liquidity costs and risks to avoid overstated profits and weak incentives for providing stable, long-term liquidity.

Practice Questions: Q2

Q2. Which of the following best describes one of the major challenges for banks in implementing an effective LTP process?

A. A decentralized LTP process is recommended to mitigate arbitrage opportunities for different business units.

B. Illiquid long-term assets should be penalized for increasing liquidity risk.

C. Performance evaluations of business unit managers should be separate from the LTP process.

D. A liquidity management information system (LMIS) should produce and monitor high-quality reports on a quarterly basis.

Practice Questions: Q2 Answer

Explanation: B is correct.

A major challenge in implementing an effective LTP process is properly accounting for the cost of liquidity in funding illiquid long-term assets and crediting business units that create benefits of liquidity through deposits. Liquidity costs, benefits, and risks should be considered in rewarding manager performance. The LMIS should create monthly reports not quarterly reports. Centralized treasury funding oversight is recommended to reduce business unit arbitrage opportunities.

Module 2. Approaches For Liquidity Transfer Pricing And Contingent Liquidity Risk Pricing

Topic 1. Approaches to Liquidity Transfer Pricing (LTP)

Topic 2. Zero-Cost: Approach

Topic 3. Zero-Cost: Disadvantages

Topic 4. Pooled Average Cost of Funds: Approach

Topic 5. Pooled Average Cost of Funds: Disadvantages

Topic 6. Separate Average Costs of Funds: Approach

Topic 7. Separate Average Costs of Funds: Disadvantages

Topic 8. Marginal Cost of Funds: Approach

Topic 9. Marginal Cost of Funds: Application

Topic 10. WAL Method

Topic 11. Contingent Liquidity Risk Pricing Process

Topic 12. Determining the Size of Liquidity Cushion

Topic 13. Challenges with Liquidity Cushion Approach Prior to GFC

Topic 14. Contingent Liquidity Risk: Example

Topic 1. Approaches to Liquidity Transfer Pricing (LTP)

-

A 2009 survey of 38 banks across nine countries identified four primary approaches to LTP:

-

zero cost,

-

pooled average cost,

-

separate average cost, and

-

matched-maturity marginal cost.

-

-

While all these approaches used the swap curve as a reference for pricing interest rate risk, they varied significantly in how they added liquidity premiums to the swap rate.

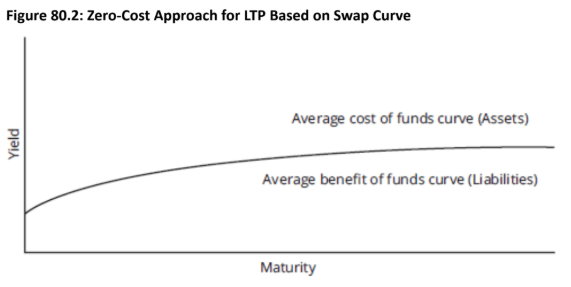

Topic 2. Zero-Cost: Approach

-

Approach: Liquidity is treated as a free good, with no costs, benefits, or risks assigned to it.

-

No charges were applied to assets for using funding liquidity, and no credits were given to liabilities for providing it.

-

The rate charged to users of funds was simply derived from the swap curve, with no additional spread for liquidity.

-

This approach led banks to accumulate balance sheets with a heavy overweighting of illiquid assets and few long-term liabilities to offset funding demands.

-

The swap curve represented both the cost of funding for assets and the credit for providing funding for liabilities, with zero premium or spread added for liquidity.

Topic 3. Zero-Cost: Disadvantages

-

Liquidity viewed as free pre-crisis: Before the GFC, some banks treated liquidity as a free good due to stable and cheap funding conditions.

-

Extremely low funding spreads: From 2005 to Q1 2007, the one-year LIBOR–swap spread averaged about 0.5 bps, making credit funding appear easy and inexpensive.

-

Liquidity risk ignored: With abundant funding, banks did not price or actively consider liquidity risk in their decisions.

-

Naïve zero-cost assumption: Some banks assumed funding would always be available at similarly low rates, reflecting an unrealistic view of liquidity.

-

Incorrect internal pricing: Assets were not charged for liquidity funding costs, and liabilities were not credited for providing liquidity.

-

Crisis-driven realization: During the 2008 crisis, the one-year LIBOR–swap spread exceeded 120 bps, highlighting that liquidity is costly and funding is not always available.

Topic 4. Pooled Average Cost of Funds: Approach

-

Approach: Interest expenses across all funding maturities are averaged and charged uniformly to liquidity users and providers.

-

Example: When funding is sourced from deposits, total interest expense across all maturities is summed and divided by total deposits, after adjusting for floats and reserve requirements.

-

Use in LTP frameworks: The pooled average approach is applied in Liquidity Transfer Pricing (LTP) to assign a single blended funding cost internally.

-

Swap curve as base: The swap rate curve is used as the reference across all maturities.

-

Asset pricing treatment: Assets are assigned a fixed spread above the swap curve across all maturities, representing the average cost of funding.

-

Liability pricing treatment: Liabilities are assigned the same average spread across all maturities, with the curve below the swap rate representing the average benefit of funds.

Topic 5. Pooled Average Cost of Funds: Disadvantages

-

Pooled average cost vs zero-cost approach: Pooled average cost is superior to the zero-cost approach, which ignores liquidity costs, benefits, and risks.

-

Disadvantages of the pooled average cost approach for LTP

-

Uniform liquidity charge

-

All assets are charged the same liquidity cost regardless of maturity.

-

Longer-term assets with higher liquidity risk are therefore undercharged.

-

-

Uniform liquidity credit

-

Liquidity providers receive the same credit irrespective of deposit maturity.

-

-

- Example: Suppose a bank uses the pooled average approach for LTP.What is likely to happen to the balance sheet if the bank decreases the liquidity spread from 9 bps to 6 bps?

-

Solution:

- Decreasing the spread would have different impacts on liabilities and assets.

- Decreasing the spread from 9 bps to 6 bps would increase the amount of loans generated as the cost of funding liquidity is significantly reduced. It would have the opposite effect on deposits because a smaller liquidity spread reduces the incentive to provide funds.

- Thus, assets wouldmost likely increase while liabilities would most likely decrease, creating an adverse effect on the loan-to-deposit ratio.

Topic 6. Separate Average Costs of Funds: Approach

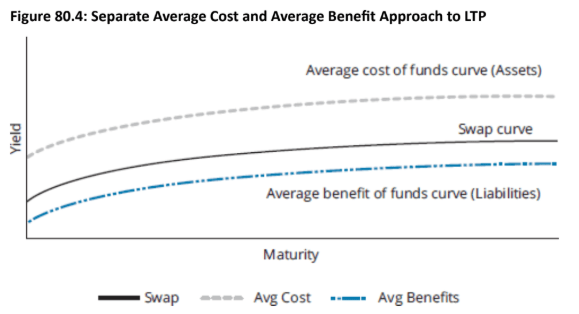

-

Approach: To address the issue in the prior example, some banks apply separate average cost of funds frameworks for assets and liabilities.

-

Distinct curves: This approach uses an average cost of funds curve for assets, and an average benefit of funds curve for liabilities, each incorporating different liquidity spreads.

-

Liability spread treatment: For liabilities, banks apply a single average spread across all maturities, rather than tenor-specific spreads.

-

Curve construction: The average benefit of funds curve is built by applying this uniform spread below the swap curve, which serves as the base across maturities.

Topic 6. Separate Average Costs of Funds: Approach

-

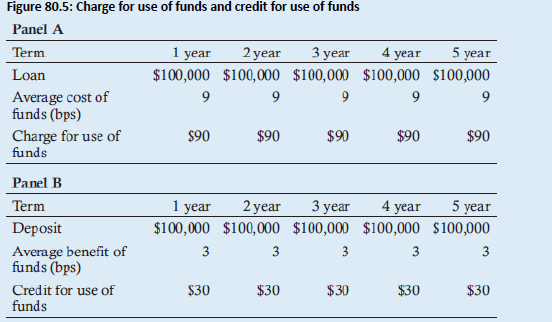

Example: Suppose a bank applies a separate average cost of funds approach for assets and liabilities at all maturities using a spread of 9 bps for all loans and a spread of 3 bps for all deposits. Under this approach:

-

What is the use of funds charge for five $100,000 loans maturing in one, two, three, four, and five years?

-

What is the credit for deposits for providing liquidity for five separate deposits of $100,000 with maturity dates in one, two, three, four, and five years?

-

What is the advantage of this approach over the pooled average cost of funds approach?

-

-

Solution: For these five loans of $100,000 each, the use of funds charge is $90 ($100,000*0.0009) regardless of the loan maturity. The providers of funding through deposits will each receive the same $30 credit regardless of maturity ($100,000 times 0.0003).

-

Advantage: Bank management can lower the funds charge on assets from 9 bps to 6 bps as an incentive to generate more loan activity without affecting the liability side of the balance sheet. The spread of 3 bps is unchanged for deposits.

-

There are several reasons that banks historically have used an average cost of funds LTP approach:

-

It is a simple process to implement, which is easier to administer because all products are charged the same spread.

-

This approach is easier for bank employees at different business units to understand and comply with.

-

A basic LMIS can be used.

-

Interest income volatility across business units is reduced using this approach because the spreads do not react as much to intermediate changes in the actual market cost of funds for the bank. This allows central management decision-makers to have more control inmaintaining group-wide objectives.

-

Topic 6. Separate Average Costs of Funds: Approach

-

Core limitation of average cost approaches (pooled or separate): A single average spread is applied across all maturities which does not reflect current market pricing of liquidity risk.

-

Incentives that increase maturity mismatch:

-

Business units are encouraged to originate more long-term loans and there is little incentive to attract long-term deposits to fund those loans.

-

This widens asset–liability maturity mismatches and raises bank liquidity risk.

-

Performance-based remuneration further amplifies this behavior, as employees target longer-term assets for higher interest income.

-

-

Impact of information asymmetry:

-

Units favor long-term loans as liquidity risk is priced the same as for short-term loans.

-

Greater incentives exist to acquire short-term deposits under the average cost approach.

-

Long-term deposits are discouraged due to insufficient compensation for longer maturities.

-

-

Distortion of profit measurement:

-

Profitability of business units is misrepresented under average cost LTP.

-

Mispricing becomes more visible during periods of market volatility.

-

The distortion is amplified because average cost approaches rely on historical, not current, market rates.

-

Topic 7. Separate Average Costs of Funds: Disadvantages

Topic 8. Marginal Cost of Funds: Approach

-

Approach: Similar in structure to the average cost of funding approach but based on current market rates rather than historical averages.

-

Reference curve

-

Typically referenced to the swap curve, constructed from the market reference rate for funding up to one year.

-

Swap rates provide a reliable term structure for estimating liquidity premiums.

-

-

Funding transformation: Fixed-rate borrowing costs are converted into floating-rate costs via internal swaps referenced to the swap curve, with the resulting spread (called liquidity premium) used to charge assets and credit liabilities for liquidity provision.

-

Risk representation: Swap curves more directly reflect market risk and idiosyncratic risk associated with interbank borrowing and lending.

-

Timeliness advantage: Using current swap rates captures the market’s current perception of funding conditions, unlike the average cost approach, which relies on lagging historical rates.

-

Best practice: The matched-maturity marginal cost of funds approach is considered the best practice for LTP.

Topic 8. Marginal Cost of Funds: Approach

-

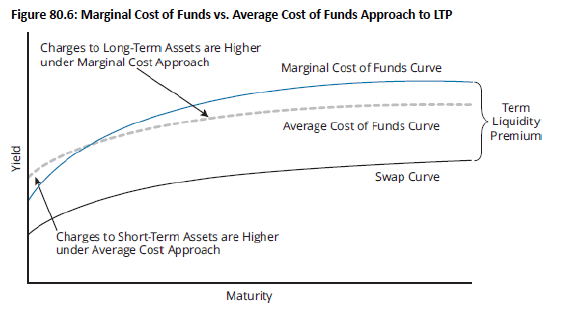

Relative shape of funding cost curves:

-

For long-term assets, the marginal cost of funds curve lies above the average cost of funds curve due to a higher liquidity (term) premium embedded in current market rates.

-

For short-term assets, the marginal cost of funds curve lies below the average cost of funds curve, reflecting a smaller term liquidity premium.

-

-

Implication for LTP: The marginal cost of funding approach is based on market rates across maturities, typically using the swap curve as the reference benchmark.

Topic 8. Marginal Cost of Funds: Approach

-

Example: Suppose a bank has fixed-rate costs associated with issuing unsecured wholesale term debt. How can the bank assign the portion associated with liquidity?

-

Solution:

-

Swapping fixed-rate costs to floating rates allows the bank to strip out the portion attributable to liquidity. The process involves stripping structured debt into embedded derivatives and floating-rate cash instruments.

-

The term liquidity premium is determined by the spread above the reference rate for the internal swap transaction at par. This liquidity premium is a better measure of the cost of liquidity than using average costs because it reflects market access premiums as well as idiosyncratic credit risks attributed to the bank.

-

Topic 9. Marginal Cost of Funds: Application

-

Most loans are repaid over time following an amortization schedule. However, a non-amortizing bullet loan is made for a fixed time period with the principal and interest being repaid in total at the end of the loan period.

-

The below example shows how the matched-maturity marginal cost approach is used for calculating the cost of funds for a non-amortizing bullet loan.

-

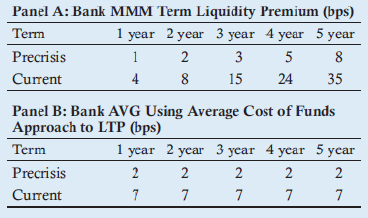

Example (Matched-maturity marginal cost approach for a bullet loan): Suppose Bank MMM uses the matched-maturity marginal cost of funds approach for LTP, and Bank AVG used the average cost approach for LTP prior to the global crisis and still uses it currently. Figure 80.7 presents the spreads used at different maturities for these two banks during these two different time periods. Suppose both banks make two non-amortizing bullet loans of $100,000 each with maturities of one and five years during both the pre-crisis and current time periods. Calculate the cost of funds for the loans of both banks during the two time periods.

-

Solution: The below fig shows comparison of Matched-Maturity Marginal Cost of Funds Approach and Average Cost of Funds Approach using pre-crisis and current spreads

Topic 9. Marginal Cost of Funds: Application

-

Solution:

-

Using Panel A , during the pre-crisis period, Bank MMM’s funding costs for the $100,000 one-year loan are 0.0001 X $100,000 = $10 and for the five-year loan are 0.0008 X $100,000 = $80. Using current costs, these same two loans from Bank MMM have a cost of 0.0004 X $100,000 = $40 and 0.350 X $100,000 = $350, respectively.

-

Using Panel B, the $100,000 one-year and five-year loans from Bank AVG using the average cost of funds approach have a funding cost of 0.0002 X $100,000 = $20 each during the pre-crisis period. These same two loans from Bank AVG have a cost of 0.0007 X $100,000 = $70, each using current costs.

-

-

Key Takeaway:

-

Underestimation under average cost approach: The example shows that using the average cost of funds significantly understates the funding cost of long-term loans, especially versus a matched-maturity marginal cost approach, with the mispricing of the liquidity premium becoming more severe during volatile periods when the price of liquidity rises.

-

Topic 9. Marginal Cost of Funds: Application

-

Amortizing loans provide principal repayments throughout their life. Because principal is gradually repaid over the life of the loan, the cost of funding the principal is not computed for its entire life.

-

Example (Matched-maturity marginal cost approach for an amortizing loan): Suppose a bank makes a $500,000 five-year loan that repays principal (and interest) with five principal repayments of $100,000 at the end of each year. Using the same spreads provided in Figure 80.7, calculate the charge for this loan using the matched maturity marginal cost of funds approach.

-

Solution: We can assume this is similar to five separate loans of $100,000 each maturing at 1, 2, 3, 4, and 5 years. This is computed using a tranching approach that is similar to calculating duration. For the pre-crisis time period, the charge is computed using the matched-maturity marginal cost approach as follows:

-

-

-

For the current time period, the charge is computed using the matched-maturity marginal cost approach as follows:

-

-

-

-

Thus, in both cases, the charge is approx the same as the charge of a bullet loan just under four years, and not the entire five-year life of the loan. Note from Figure 80.7 that a bullet loan for four years would have a charge of 5 bps and 24 bps for the two time periods, respectively.

\frac{1(1)+2(2)+3(3)+4(5)+5(8)}{1+2+3+4+5}=\frac{74}{15}=4.9 \text{ bps }

\frac{1(4)+2(8)+3(15)+4(24)+5(35)}{1+2+3+4+5}=\frac{336}{15}=22.4 \text{ bps }

Topic 10. WAL Method

-

Uncertain cash flows: Not all amortizing loans have predictable repayments, as cash flows can vary due to borrower behavior.

-

Mortgage example: Variable-rate mortgages with long contractual maturities (e.g., 25–30 years) are often repaid early due to home sales or relocations.

-

Behavior-based grouping: Similar loans are bundled by origination tenor when their repayment behavior is broadly comparable.

-

WAL approach: This grouping method is known as the weighted-average life (WAL) approach for determining funding charges based on expected behavior and maturity.

-

Definition: WAL measures the weighted-average time required to recover $1 of principal.

-

Formula: The charge for the entire portfolio is computed as:

-

-

: principal amount in distribution

-

: amount of loan

-

: years of payment i

-

- Example: Suppose in an average month a bank writes $1 billion of 15-year amortizing loans. Based on the behavior of past customers who often repay the entire balance early, the bank assumes the repayment of the principal for the portfolio will be closer to 8 years. Assume that the current rate for the matched-maturity approach of funding cost is 58 bps. Calculate the dollar cost of this charge for the entire portfolio.

- Solution: The charge to this business unit for the entire $1 billion portfolio is 58 bps. The dollar cost of this charge would be 0.0058 X $1 billion = $5.8 million.

\mathrm{WAL}=\sum_{\mathrm{i}=1}^{\mathrm{n}} \frac{\mathrm{p}_{\mathrm{i}}}{\mathrm{P}} \mathrm{t}_{\mathrm{i}}, \text{ where }

p_i

t_i

P

Topic 10. WAL Method

-

Deposits are categorized as sticky or hot/volatile based on the likelihood of customers withdrawing the funds.

-

Examples of sticky deposits are term deposits for a prespecified maturity.

-

Examples of hot or volatile deposits are demand deposits, savings, and transaction accounts that can be fully withdrawn at any point in time.

-

- Example (Calculating the credit for the liquidity benefit of deposits): Suppose the two banks described in the previous example, Bank MMM and Bank AVG, each have two $100,000 deposits with one-year and five-year terms. Using the same information provided in Figure 80.7, what should be the credit given to business units that acquire deposits with one-year and five-year terms, both prior to the crisis and currently, using the two approaches for cost of funding?

-

Solution:

- The business unit for Bank MMM using the matched-maturity marginal cost of funds approach for LTP would give a credit prior to the crisis of $10 for the one-year and $80 for the five-year term deposits. Using current bps spreads, the business unit for Bank MMM would give a credit of $40 and $350 for the one-year and five-year term deposits, respectively.

- The business unit for Bank AVG, using the average cost of funds approach for LTP, would give a credit prior to the crisis of $20 each for the one-year and five-year term deposits. Using current bps spreads, the business unit for Bank AVG would give a credit of $70 each for both deposits regardless of the term.

Practice Questions: Q1

Q1. Which of the following statements describes the best approach for liquidity transfer pricing?

A. Zero cost of funds approach is preferred in cases in which swap rates are unknown and undeterminable.

B. The pooled average cost of funds approach is more appropriate for banks with numerous business units.

C. The separate average cost of funds approach is preferred to accurately account for business units with large trading activities.

D. The matched-maturity marginal approach is preferred because it quantifies liquidity risk premiums across all maturities.

Practice Questions: Q1 Answer

Explanation: D is correct.

The best practice for LTP is the matched-maturity marginal cost of funds approach. This approach uses the bank’s actual market cost of funding to calculate the correct portion to liquidity.

Topic 11. Contingent Liquidity Risk Pricing Process

-

Global liquidity standards: The BCBS introduced two global liquidity risk metrics: the Liquidity Coverage Ratio (LCR) and the Net Stable Funding Ratio (NSFR).

-

LCR purpose: LCR requires banks to hold sufficient high-quality liquid assets to withstand net cumulative cash outflows from idiosyncratic shocks over a 30-day stress period.

-

NSFR purpose: NSFR addresses structural liquidity risk by encouraging stable, longer-term funding to support illiquid long-term assets.

-

Behavioral and systemic impact: Together, LCR and NSFR aim to make banks more self-sustainable, increase liquidity cushions against unexpected funding outflows, and reduce reliance on central banks as lenders of last resort during crises.

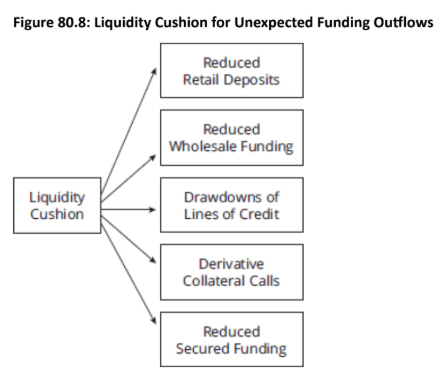

Topic 12. Determining the Size of Liquidity Cushion

-

Stress Testing & Scenario Analyses: It is recommended to use stress tests and scenario analyses to determine the size of liquidity cushion, accounting for bank-specific complexity and scale, and covering both idiosyncratic and systemic shocks over prolonged market disruptions.

-

Composition of the cushion: In line with BCBS guidance, meet LCR requirements with highly liquid assets (e.g., cash and government securities), not short-term funding such as overnight sources.

-

Funding structure: Rely on longer-term deposits to withstand extended periods of market stress and funding disruption.

-

Cost attribution: Treat the liquidity cushion as a cost of doing business and allocate it to business units, with higher contingent liquidity charges for activities with greater likelihood of unexpected funding outflows.

Topic 13. Challenges with Liquidity Cushion Approach Prior to GFC

-

Before the GFC, many banks just charged assets an average cost of funding for the bank carrying additional liquidity at the overnight funding rate.

-

There are several problems with this approach:

-

This approach incorrectly assumes all assets have the same contingent liquidity risk.

-

Only charging assets ignores the fact that liabilities have run-off risk related to reduced deposits and off-balance-sheet risks such as additional drawdowns on lines of credit.

-

It does not match the liquidity risk with the probability of liquidity usage by different business activities.

-

The liquidity charge is not measured granular enough to discourage the use of products that have more contingent liquidity risk.

-

Topic 14. Contingent Liquidity Risk: Example

-

Example: Suppose a bank supplies a line of credit of $20 million that currently has a balance of $5 million outstanding. Based on the customer’s transaction history, projected needs, and credit score, the bank determines that there is a 70% probability the customer will use the $15 million remaining line of credit. The bank’s cost of funding for the liquidity cushion is 15 bps. If the bank charges contingent commitments based on the probability of a drawdown, calculate the charge for liquidity for this line of credit.

-

Solution: The rate charged for the contingent commitment is determined as:

-

-

Multiplying this cost by the $20 million credit line amount yields a dollar cost of

$15,750.

\begin{aligned}

\text{Contingent liquidity charge} &= \frac{\text{(remaining balance)}}{\text{(credit limit)}} \times \text{probability of drawdown} \times \text{liquidity cushion cost of funding}\\

\text{Contingent liquidity charge} &= \frac{\$ 15 \text{ million}}{\$ 20 \text{ million}}\times 70 \%\times 0.0015=0.000788 \text{ or 7.88 bps}

\end{aligned}

Practice Questions: Q2

Q2. A bank supplies a line of credit of $10 million that currently has $6 million already drawn. The bank determines that there is a 65 % probability the customer will use the remaining line of credit. The bank's cost of funding for the liquidity cushion is 16 bps . If the bank charges contingent commitments based on the probability of a drawdown, what should the charge for liquidity be for this line of credit?

A. $1,664.

B. $2,496.

C. $4,160.

D. $5,850.

Practice Questions: Q2 Answer

Explanation: C is correct.

The rate charged for the contingent commitment is determined as follows:

Multiplying this cost times the $10 million credit line amount yields a dollar cost

of $4,160.

\begin{aligned}

\text { Contingent Liquidity Charge }&= \frac{\text {Remaining Balance}}{\text {Credit Limit}} (\text {Probability of Drawdown}) \times \text { (Liquidity Cushion Cost of Funding)} \\

&= \frac{\$ 4 \text { million }}{\$ 10 \text { million }} \times (65 \%) \times (0.0016) \\

&= 0.000416 \text { or } 4.16 \text{ bps}

\end{aligned}

Copy of LTR 14. Liquidity Transfer Pricing

By Prateek Yadav