Costs in the

Short Run and Long Run

Christopher Makler

Stanford University Department of Economics

Econ 50 : Lecture 15

Today's Agenda

- Review of Econ 1 Treatment of Production and Cost

- Total, Average, and Marginal Costs

- Long-Run Costs and Returns to Scale

- Short-Run Costs and the Marginal Product of Labor

The Econ 1 Approach

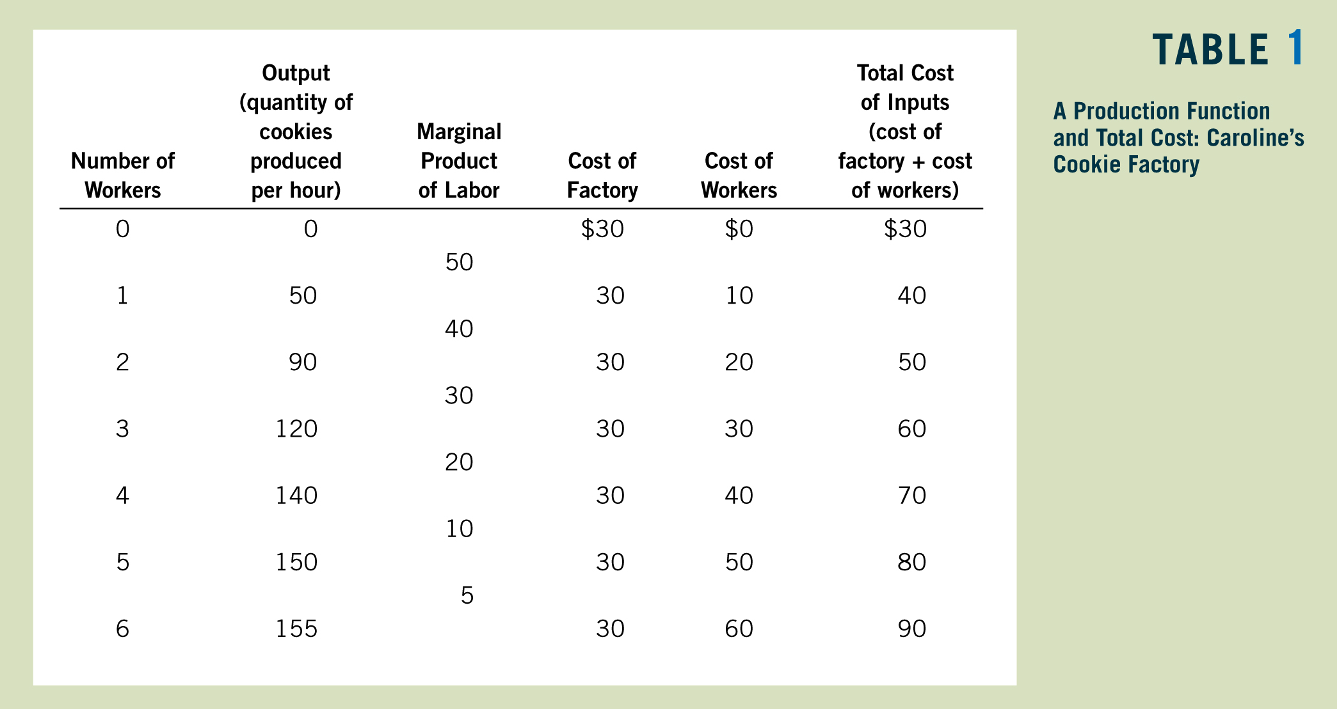

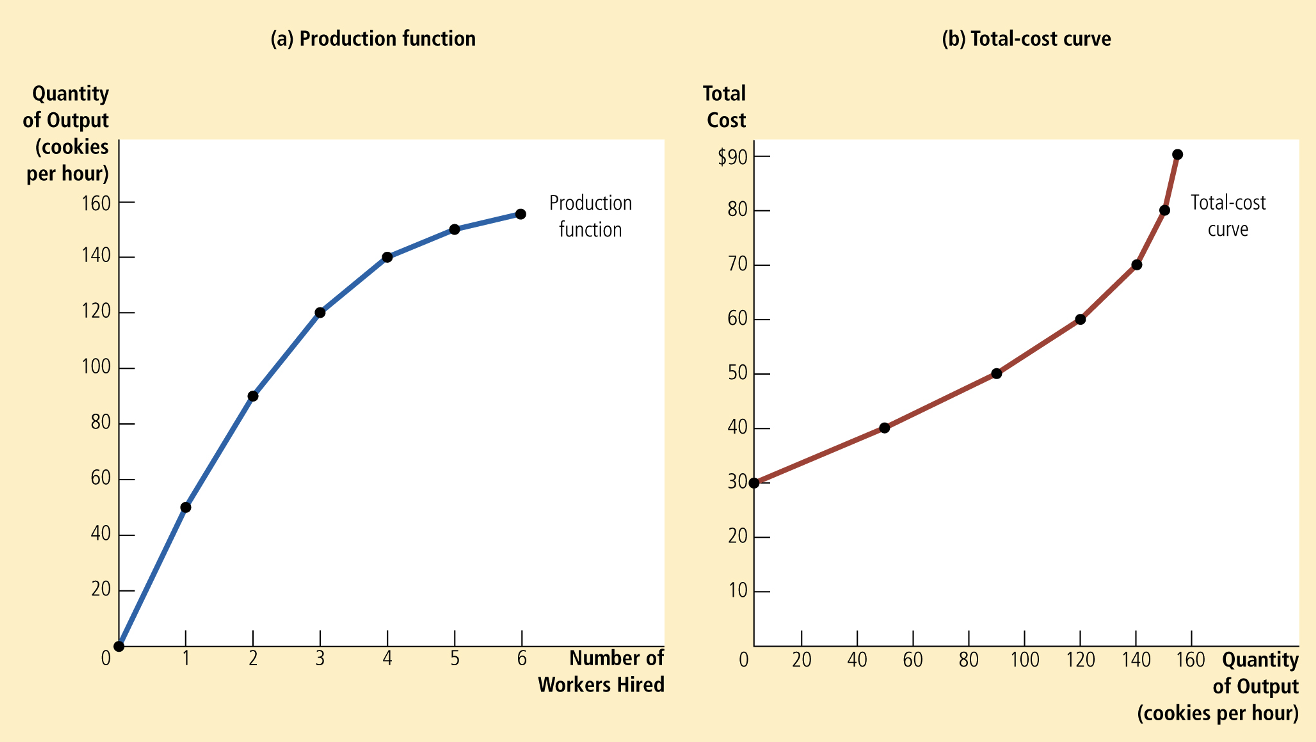

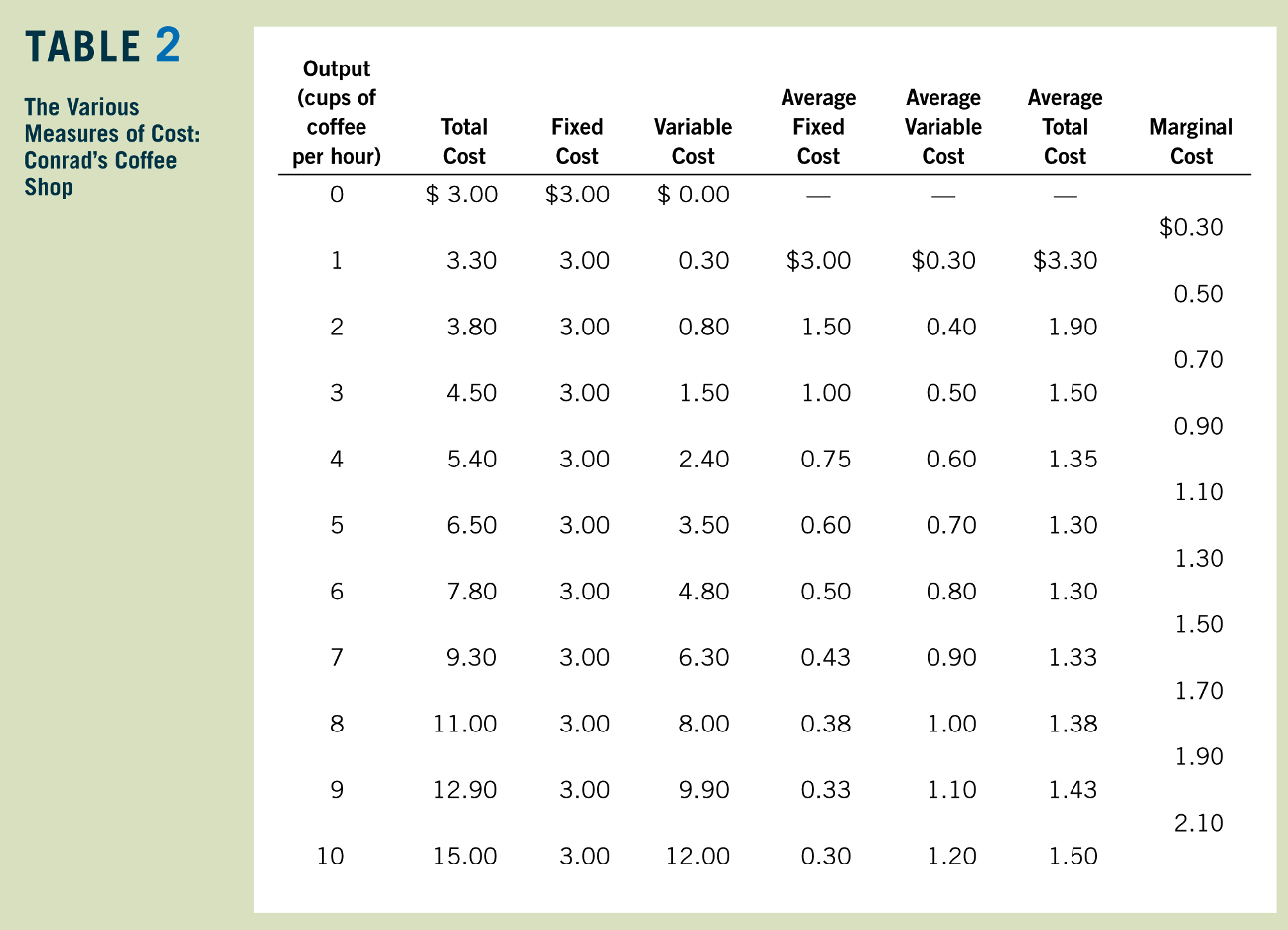

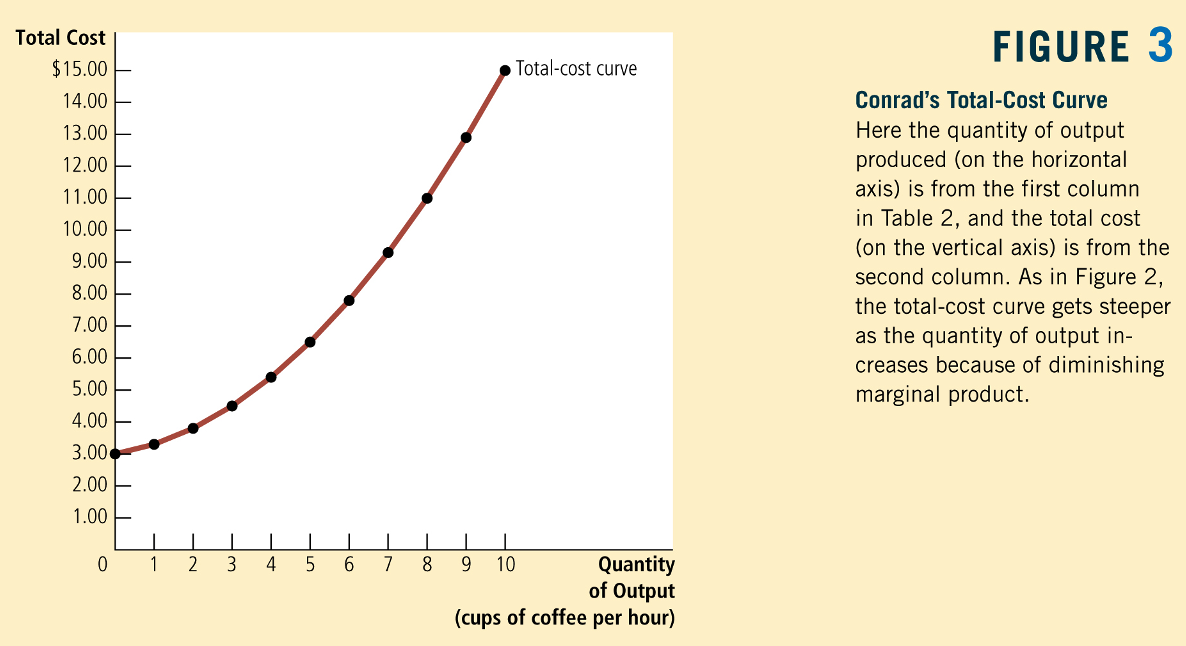

Greg Mankiw, Principles of Economics

Greg Mankiw, Principles of Economics

Greg Mankiw, Principles of Economics

Greg Mankiw, Principles of Economics

Greg Mankiw, Principles of Economics

Dollars

Dollars Per Unit

Greg Mankiw, Principles of Economics

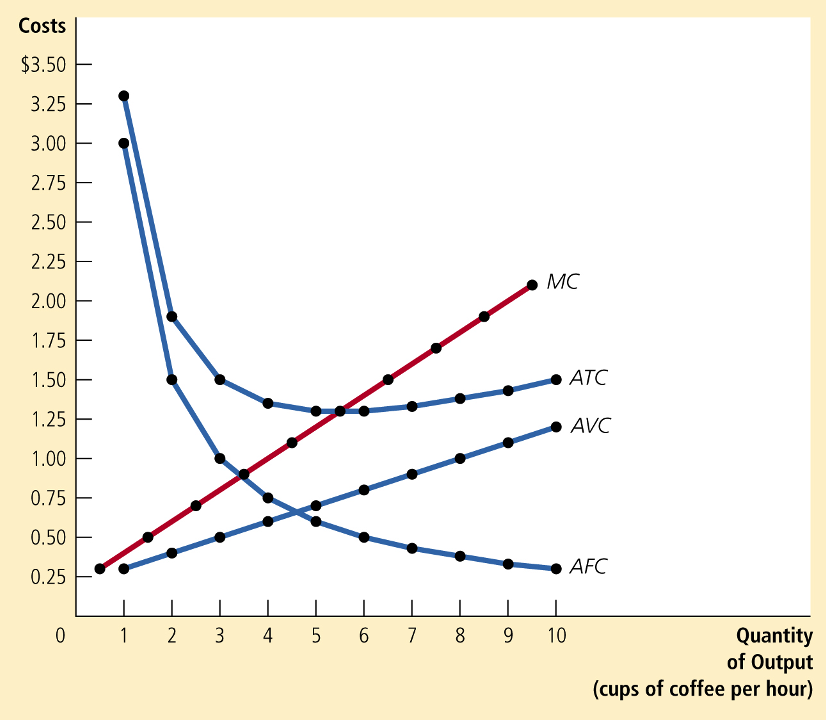

Total, Average, and Marginal Costs

Total Cost:

Average Cost:

Marginal Cost:

Suppose it costs $100,000 to fly 200 passengers from SFO to NYC

Marginal cost tends to "pull" average cost toward it:

Marginal grade = grade on last test, average grade = GPA

Relationship between Average and Marginal Costs

pollev.com/chrismakler

Suppose q* is the quantity

for which ATC is lowest.

Which of the following must be true?

(Assume that ATC and MC are continuous functions of q.)

(a) MC also reaches its minimum at q*

(b) MC reaches its maximum at q*

(c) MC and ATC are equal at q*

Long-Run Costs

From Last Time: Cost Minimization

Subject to an Output Constraint

Conditional Demand

Expansion Path

A graph connecting the input combinations a firm would use as it expands production: i.e., the solution to the cost minimization problem for various levels of output

Assuming the optimum is found via a tangency condition,

exactly the same as the tangency condition.

Long-Run Total Cost of \(q\) Units

Conditional demand for labor

Conditional demand for capital

"The total cost of producing \(q\) units in the long run

is the cost of the cost-minimizing combination of inputs

that can produce \(q\) units of output."

Returns to Scale and Long-Run Cost Functions

From last time: what happens when we increase all inputs proportionally?

For example, what happens if we double both labor and capital?

Does doubling inputs -- i.e., getting \(f(2L,2K)\) -- double output?

Decreasing Returns to Scale

Constant Returns to Scale

Increasing Returns to Scale

Decreasing Returns to Scale

Constant Returns to Scale

Increasing Returns to Scale

pollev.com/chrismakler

When does the production function

exhibit constant returns to scale?

Decreasing Returns to Scale

Constant Returns to Scale

Increasing Returns to Scale

Consider the Cobb-Douglas production function

If we double both labor and capital, we get

How does this compare to double the output?

Consider the Cobb-Douglas production function

\(\theta\) is a constant that depends on \(a\), \(b\), \(w\), and \(r\)...but we're actually just interested in the exponent on \(q\) for right now

The long-run cost function for this is

Decreasing Returns to Scale

Constant Returns to Scale

Increasing Returns to Scale

Consider the Cobb-Douglas production function

The long-run cost function for this is

Decreasing Returns to Scale

Constant Returns to Scale

Increasing Returns to Scale

- decreasing returns to scale: the long-run total cost curve will get steeper as you produce more output: i.e., you have increasing marginal and average costs.

- If the production function has constant returns to scale, the long-run cost total cost curve will be linear; marginal and average costs are constant.

- increasing returns to scale results in lower costs as you produce more.

Short-Run Costs

Now assume that the level of capital is fixed in the short run at some amount \(\overline K\).

The amount of labor required to produce \(q\) units of output is therefore also going to depend upon \(\overline K\):

Scaling Production in the Short Run

Suppose \(K\) is fixed at some \(\overline K\) in the short run.

Then the production function becomes \(f(L\ |\ \overline K)\)

pollev.com/chrismakler

When does the production function

exhibit diminishing marginal product of labor?

Short-Run Expansion Path

- Shows how the firm's choice of labor and capital changes as it expands production.

- If capital is fixed, what does this look like?

Short-Run Total Cost of \(q\) Units

Variable cost

"The total cost of producing \(q\) units in the short run is the variable cost of the required amount of the input that can be varied,

plus the fixed cost of the input that is fixed in the short run."

Fixed cost

Short-run conditional demand for labor

if capital is fixed at \(\overline K\):

Total cost of producing \(q\) units of output:

Total, Fixed and Variable Costs

Fixed Costs \((F)\): All economic costs

that don't vary with output.

Variable Costs \((VC(q))\): All economic costs

that vary with output

explicit costs (\(r \overline K\)) plus

implicit costs like opportunity costs

e.g. cost of labor required to produce

\(q\) units of output given \(\overline K\) units of capital

pollev.com/chrismakler

Generally speaking, if capital is fixed in the short run, then higher levels of capital are associated with _______ fixed costs and _______ variable costs for any particular target output.

Fixed Costs

Variable Costs

Average Fixed Costs (AFC)

Average Variable Costs (AVC)

Average Costs

Average Costs

Fixed Costs

Variable Costs

Marginal Cost

(marginal cost is the marginal variable cost)

Marginal Cost

Relationship between Marginal Cost and Marginal Product of Labor

Comparing the Short Run and the Long Run

Returns to a Single Input

- Increasing marginal product: MPL is increasing in L

- Constant marginal product: MPL is constant in L

- Diminishing marginal product: MPL is decreasing in L

Returns to Scale (Scaling all inputs.)

- Increasing returns to scale: doubling all inputs more than doubles output.

- Constant returns to scale: doubling all inputs exactly doubles output.

- Decreasing returns to scale: doubling all inputs less than doubles output.

Long Run (can vary both labor and capital)

Short Run with Capital Fixed at \(\overline K \)

Long Run (can vary both labor and capital)

Short Run with Capital Fixed at \(\overline K \)

Let's fix \(w= 8\), \(r = 2\), and \(\overline K =32\)

Relationship between

Short-Run and Long-Run Costs

What conclusions can we draw from this?

Summary and Next Steps

- Today: derive the long-run and short-run total cost functions and associated unit cost curves for a firm

- Next week: embed this into the profit maximization problem and solve for the optimal output level \(q^*\)